![]() When initially calling on a Wednesday, I spoke with a gentleman named Juan Regarding closed/charged off accounts on my credit report. He was very professional, and walked me through... read more

When initially calling on a Wednesday, I spoke with a gentleman named Juan Regarding closed/charged off accounts on my credit report. He was very professional, and walked me through... read more

Robert G.

Robert G.4/05/2024

![]() I recently reached out to IMAX Credit Repair to address several credit issues, notably a number of credit card accounts in collections. My experience with them, especially with Elizabeth, was... read more

I recently reached out to IMAX Credit Repair to address several credit issues, notably a number of credit card accounts in collections. My experience with them, especially with Elizabeth, was... read more

1/18/2024

![]() Ali and his team are the best. Not only are they sweet and professional they really keep you updated throughout the process. They have helped me twice my entire life... read more

Ali and his team are the best. Not only are they sweet and professional they really keep you updated throughout the process. They have helped me twice my entire life... read more

12/24/2023

![]() I reached out to Ali Zane several months ago and he is the real deal. I am super satisfied with his expertise and he has earned my trust. Don't waste... read more

I reached out to Ali Zane several months ago and he is the real deal. I am super satisfied with his expertise and he has earned my trust. Don't waste... read more

Tim A.

Tim A.10/08/2022

![]() I've had the good fortune of being assisted by Ali in the past & would HIGHLY recommend him & his associates.

I've had the good fortune of being assisted by Ali in the past & would HIGHLY recommend him & his associates.

William V.

William V.7/22/2022

![]() Ali is the best! He really takes his time explaining to you how you can fix your credit. A family member recommended him to me and he didn't disappoint. Building/fixing... read more

Ali is the best! He really takes his time explaining to you how you can fix your credit. A family member recommended him to me and he didn't disappoint. Building/fixing... read more

Denise K.

Denise K.1/21/2022

![]() I was referred to IMAX credit by another credit repair firm in regards to removing late payments that were on my account. I scheduled a free consultation with Ali. Ali... read more

I was referred to IMAX credit by another credit repair firm in regards to removing late payments that were on my account. I scheduled a free consultation with Ali. Ali... read more

5/29/2021

![]() Ali and Samantha are the best team! My credit score was stunned last year and I spent months working with the bank myself without a result. I was... read more

Ali and Samantha are the best team! My credit score was stunned last year and I spent months working with the bank myself without a result. I was... read more

Rose Y.

Rose Y.5/05/2021

![]() Ali is amazing! Ali and Samantha were able to restore my FICO score to where the score should have been all along. I had one small ding due to an... read more

Ali is amazing! Ali and Samantha were able to restore my FICO score to where the score should have been all along. I had one small ding due to an... read more

3/31/2021

![]() I moved and unintentionally missed my final utility bill. A few months later a late payment popped on my credit report. I consulted with Ali. He was... read more

I moved and unintentionally missed my final utility bill. A few months later a late payment popped on my credit report. I consulted with Ali. He was... read more

Daniel K.

Daniel K.3/04/2021

The Most Effective Credit Bureau Dispute Letter

This blog post is for the people who cannot afford my paid credit repair services in Los Angeles and prefer a self help strategy.

So, I’ve distilled my 20 years of experience of fixing credit scores into an advanced method credit bureau dispute letter with specific instructions on how to utilize it.

Here’s what you need to know: The Fair Credit Reporting Act’s (FCRA) Section 611 allows for consumers to challenge questionable items on their credit reports. So you have a right to dispute information that you believe to be incorrect.

This includes questionable late payments charge-offs, collections, tax liens, bankruptcies, judgments, foreclosures, or any personal identification information.

What this means is, virtually any “questionable” negative or inaccurate information the credit bureaus (also known as credit reporting agencies) have for you can be disputed and their deletion may result in a credit score increase.

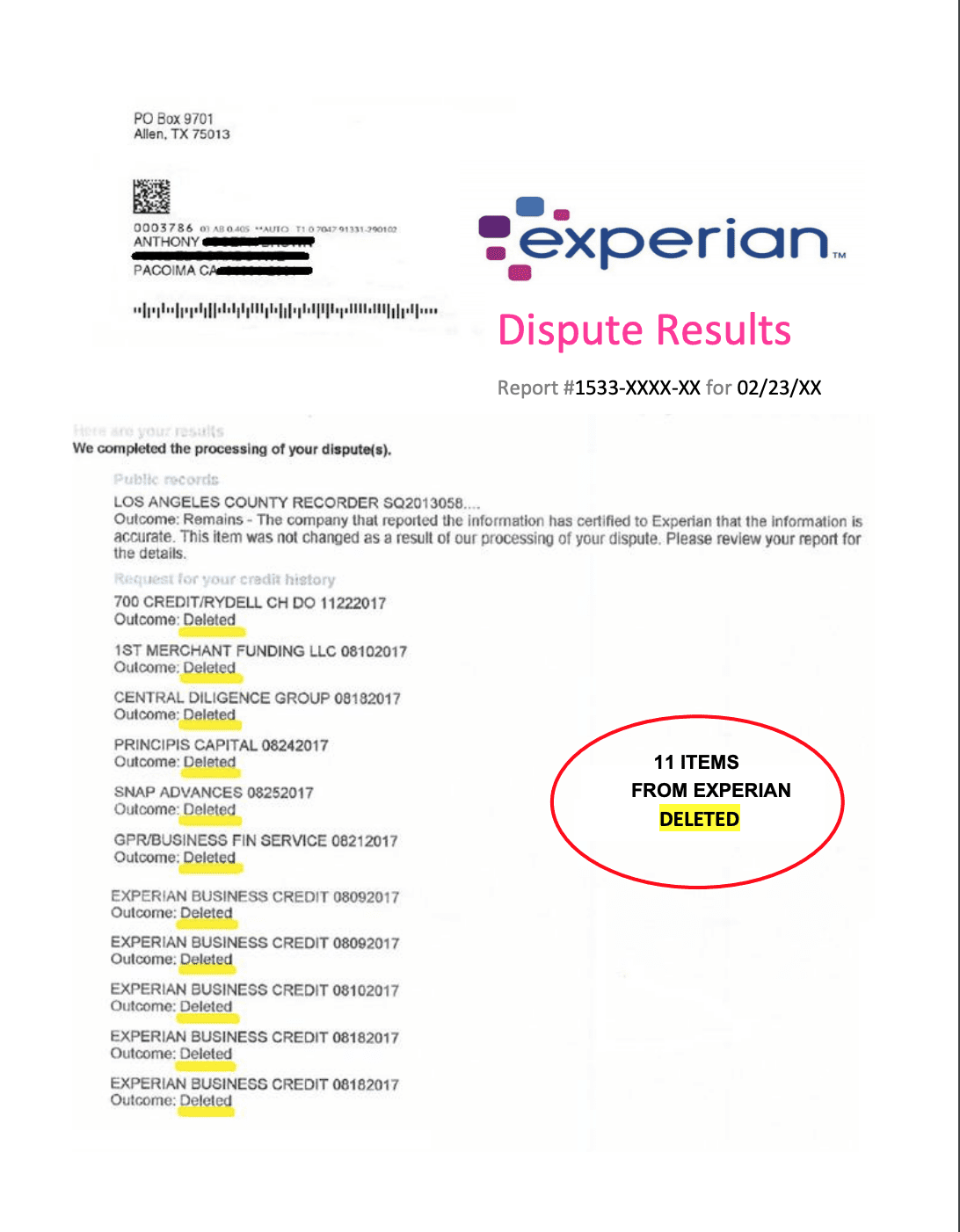

Proof this letter works, Check out these results I’ve got for my clients!

These are actual confirmation of removal of accounts from the credit bureaus:

Want more proof?

Check out our Yelp Reviews.

Now, let’s start with the basics.

Sample credit bureau dispute letter :

Here is a free dispute letter sample that works:

Full Name_____

Mailing Address:________

Date of Birth________

{Date}_______

RE: Investigation Request to Delete Credit Inquires

To whom it may concern,

In accordance with the Fair Credit Reporting Act Section 611 (15 U.S.C. § 1681I), I am practicing my right to challenge questionable information that I have found on my personal credit report. I do not recognize the information listed below and request that you investigate the source of these accounts and ascertain that the creditor had a permissible purpose, and is able to verify my complete file information including full name, address, date of birth and SSN#.

INCORRECT ACCOUNT INFORMATION

The accounts below are reporting incorrectly please investigate these:

1. {Creditor Name}________ {ac#} _______{Reason for Dispute}_________

2. {Creditor Name}________ {ac#}________ {Reason for Dispute}__________

3. {Creditor Name}________ {ac#}________ {Reason for Dispute}___________

INCORRECT CREDIT INQUIRIES

I am disputing the following inquiries which I did not authorize:

1. {Creditor Name}_______ {inquiry date}_______

2. {Creditor Name}_______ {inquiry date}_______

REMOVE INCORRECT PERSONAL INFORMATION

I am disputing the following personal information that is showing for me which is incorrect:

1. Incorrect SSN {xxx-xx-xx xx }______

2. Incorrect Address { insert address}_________

3. Incorrect Name Variations { Insert name}________

UPDATE PERSONAL INFORMATION

Also please update the following information which I saw your credit bureau to be missing or incomplete:

1. Personal current address {insert correct address}__________

2. My proper full { insert your correct full name, if the bureau has listed it incorrectly}________

3. My date of birth { insert date of birth, if bureau has it listed incorrectly}_________

4. My current employment info { insert employer name, address and your position, if the bureau is missing this info}__________

I am allowing you 30 days to complete this investigation after which I authorize you to mail me my updated credit reports along with the investigation results

Truly,

{Name}______

{Signature}____________

Experian Address for disputes:

If Sending to Experian:

Mail to Experian, P.O. Box 4500, Allen, TX 75013

Equifax Address for disputes:

If Sending to Equifax

mail to : Equifax P.O. Box 740256, Atlanta, GA 30374-0256}

Transunion Address for disputes:

If Sending to Transunion:

mail to : Transunion, Consumer Disputes, P.O. Box 2000, Chester, PA 19016

How to write a credit bureau dispute letter:

Use the credit dispute letter template provided above. Fill in with your personal and account information using the steps below:

STEP 1: Identify yourself

Fill in: your personal identification information, current address, date of birth, and SSN.

STEP 2: Choose items to dispute

List the erroneous personal identification information you are disputing along with a list of the questionable accounts and inquiries.

For each account, list the creditor name and the account number, along with the reason for your dispute.

Best dispute reasons to use with a credit bureau dispute letter:

Examples of dispute reasons you can use are follows:

The Account does not belong to me.

The account payment history is incorrect.

The account is too old to be on the credit report.

The account was paid prior to collection.

Incorrect amount.

Incorrect last payment date.

Incorrect Status.

The account belongs to someone else with a similar name.

Creditor agreed to delete account from credit report.

What Items to enclose with the credit bureau dispute Letter

The credit bureaus require you to verify your identity in order for them to investigate and send you dispute results back

–Photo ID: This could be any state or government-issued identification

–Proof of Residency: This could be a recent utility bill, or bank statement, mortgage statement, or a copy of your home rental agreement. It should show your name and current mailing address.

— Proof of SSN#: This could be any state or government document showing your SSN#. Or a page from your tax return, W-2, paystub, or 1099, etc.

Any Supporting Documentation: This could include anything that could support your dispute claim, like a letter of deletion from the creditor.

Wait for 30 Days for the Dispute Completion:

Within 30 days after receipt of the letters by the bureaus, you should receive the investigation results from them.

SIMILAR READ: How to Remove Charge-Offs from a Credit Report

The results will show what accounts were disputed and whether they were deleted, updated with new information, or remain unchanged. Learn more about how to remove dispute comments.

How to dispute accounts with credit bureaus: Phone, Mail, Online or Fax?

Most consumers dispute accounts by phone or online.

This is a huge mistake!

The three major credit bureaus, Experian, Equifax, and Transunion, allow you to pull a free credit report directly from their websites every 12 months, or from annualcreditreport.com, or through sites like CreditKarma.

Those reports will provide you with a link to dispute online and a phone number for the credit bureau’s customer service dispute center. (Learn more about how to contact credit bureaus here)

Phone and online disputes, although maybe the simplest ways to dispute. Any serious credit repair expert will tell you never to use this method.

Why? Consumers are at a disadvantage every time they do this.

Firstly, the credit bureaus make consumers agree to innocuous-sounding waivers, which in fact make clients give up their rights to re-investigation.

Second, without a proper paper trail, the credit bureaus do not have to fear the threat of lawsuits. So the bureaus can take online and phone disputes less seriously.

This means less thoroughly investigated disputes that lead to items not being deleted from the credit report.

So using an actual credit dispute letter and mailing or faxing will serve you much better.

Watch this video to understand your state and federal rights, and how to utilize them to protect yourself and repair your credit:

Common mistakes to avoid with credit dispute letters

So over the years, I’ve seen clients of mine make errors that end up hurting their chances for deletion.Here are ways to avoid these mistakes:

C) Do not dispute any inquiries linked to accounts you’ve legitimately opened, your inquiry dispute will be forwarded to the creditor, who may close the account fearing fraud.

D) Make sure to include entire account numbers if the same creditor is reporting multiple accounts. You do not want the wrong account disputed and deleted.

What accounts you should never challenge with credit bureaus

I absolutely cannot stress this enough; When trying to repair your credit, DO NOT dispute any legitimate debts that fell behind recently, which you cannot afford to pay off.

Here’s why – Creditors can legally sue consumers within the statute of limitations they are allowed by the state the debtor resides in.So, check the statute of limitation for debts in your states before disputing any large unpaid accounts.

For example in California, the statute of limitations for debts is 4 years.

Here’s what this means: If you live in California, creditors can sue you for up to 4 years from the time you defaulted on a debt. Disputing accounts that lie within the statute of limitations may incite the creditor to take legal action against you. But this does not pertain to items that are resulting from identity theft.

What type of accounts can you remove with a credit report dispute letter:

You can dispute the following questionable items:

Credit account-related Disputes: Charge-offs, late payments, missed payments, collections (including medical bills), repossessions, student loans, installment loans, auto loans, mortgage foreclosures. Virtually any account that is reporting on your credit file.

Public records: These include, IRS tax liens, state tax liens, judgments, and bankruptcies.

Credit Inquiries: Requests for your personal credit report, aka credit inquiries, are recorded by the credit bureaus and kept on record for 2 years. You can dispute credit inquiries that are questionable and improve your credit scores by getting them deleted.

Personal information: You can dispute to get removed or have the bureaus update all your personal information including your name, current address and previous addresses, your phone number, your employment information, your date of birth, and SSN#.

How to dispute recent late payments and recent collections

Something you must know – Any recent collection, or recent late payments, cannot be removed from your credit report with a credit bureau dispute letter.

How to remove these:

Recent late payments: For recent late payments within the last 2 years or on open accounts, the only way to get these expunged is by utilizing the direct creditor dispute method. For older late payments, the credit bureau dispute letter would work.

Recent collection accounts: For recent collection accounts, which fell behind within the last 4 years that are valid, the most effective way to get these expunged is to utilize the pay for delete method, where you offer to settle the account in exchange for deletion from your credit report.

Older collection accounts: Or for re-aged collection accounts, you’ll need a debt validation letter, where you challenge the debt with the debt collector first.

After the collection company receives your letter, only then should you send out a credit bureau dispute letter. This way the collector is being asked for verifications on two fronts, by you directly and from the bureaus as well.

What to do if the credit bureaus do not correct your credit report

Sometimes the bureaus won’t send you the investigation results, as they may deem your identification information incomplete.

Regardless, they are required to investigate the items you requested.

So, here’s what you do:

Pull your updated credit report after about 35 days from the time you mailed out the dispute letters.

Then check on each bureau if there have been any deletions or any accounts showing they are “under re-investigation.”

These two indicators should let you know if the bureaus actually investigated your claim or not.

If you find no such indicators, refer back to your certified mail tracking information and confirm the bureaus received the letters.

If the letters were received, then you can move to lodge complaints against the bureaus, as discussed below.

How to file regulatory complaints against the bureaus and creditors:

In the event that the bureaus do not investigate or correct your credit report,

Then you take more extreme measures…

You lodge a regulatory complaint with the Consumer Financial Protection Bureau (CFPB) at www.consumerfinance.gov.

What’s great about the CFPB is, you can also lodge complaints against creditors and collection companies here.

The CFPB forwards these complaints to the party you lodge a complaint, who must respond back to the CFPB within 30 days with a resolution.

They also collects data on the number of complaints filed against each institution and may take regulatory action against them if they notice a pattern of violations.

Using the Section 604 dispute letter/ Method of Verification Letter

Now if the CFPB compliant doesn’t do the trick

Here’s what you do then:

You exercise your right under the FCRA Section 609 and Section 604 to request a method of verification.

Through another important tool known as the section 609 dispute letter or section 604 dispute letter, both dispute letters are similar.

This is how it works – you’re asking the creditors to provide you with details pertaining to how and with whom they verified the information you disputed.

The sample method of verification letter

Here is the template for the Method of verification letter:

Full Name

Mailing Address:

Date of Birth

{If Sending to Experian: P.O. Box 4500, Allen, TX 75013}

{If Sending to Equifax: P.O. Box 740256, Atlanta, GA 30374-0256}

{If Sending to Transunion: Consumer Disputes, P.O. Box 2000, Chester, PA 19016}

{Date}

RE: Investigation Request to Delete Credit Inquires

I sent your company my dispute on {Date}, which you received and investigated on. I have reason to believe that you conducted a reasonable investigation. therefore, I am invoking the Fair Credit Reporting Act Section 611 to ask that you provide me with the following information:

1. The date you contacted the creditor

2. The contact information for the creditor

3. The name of the person who verified the item to you

4. The method of communication you used to verify this information

5. Did the creditor provide you with my SSN, address, and Date of Birth?

I am allowing you 30 days to complete this investigation after which I authorize you to mail me my updated credit reports along with the investigation results

Truly,

{Name}

{Signature}

If credit bureau disputes are not successful, seek professional help :

Now credit bureau disputes are not the end all solution for credit repair and often don’t remove all negative items.

Hence, some cases require professional and legal help, especially when a handful of stubborn items are keeping your score down

Over the last 20 years, I have helped my clients remove hundreds of late payments from their records.

Reach out if you’d like to see if I can help you too!

143 Comments. Leave new

Hi,

I have an installment loan that was predatory from 5 years ago. I live in California, I have since found out that the loans are illegal in California. They were not illegal when I took out the loan but they are now. Can I use that leverage in a dispute letter?

Hi Alicia, that’s something that would need legal intervention, where you’re taking this up directly with the auto loan company.. All the credit bureaus do is check for accuracy but the credit bureaus don’t determine if something is predatory or not.

I recently incurred a 30 day late payment on my credit with Synchrony bank , what can I do regarding that, will this letter work?

Hi Harry, for recent late payments, the only way to remove a late payment is if a creditor agrees to remove the late payment. And this is often a complicated process.

Here’s an article about this I’ve written: https://www.imaxcredit.com/how-to-remove-a-30-day-late-payment-from-the-credit-report/

After reading it and if you still need help reach out to our team for a free consult

Hello,

I was recently sued by a creditor and the case was dismissed. I was under the impression that this would come off my credit report in 30 -90 days. How should I start the dispute process to get this removed? Or which letter template should I use?

He Becca, unfortunately if a lender sues and the case is dismissed it doesn’t have anything to do with the credit reporting.

Yes you can dispute the item, look through the credit reporting and see what’s inconsistent across the 3 bureaus and point that out in the disputes.

Thank you for your post. I really enjoyed reading it, especially because it addressed my issue. It helped me a lot and I hope it will also help others.

appreciate the kind words !!! Best of luck in your credit journey

Hello , I’ve been recently trying to get a few accounts off, which shouldn’t be there.These are paid collections. I’ve disputed them numerous times but to no avail. I’ve called the collection companies Midland Credit Managment and Portfolio Recovery and was told that they have instructed the bureaus to remove them, however at my end the accounts are still showing , what can I do ?

Hi Lucy, I understand you’ve already disputed these accounts but to no avail

I’d be curious to know what the bureaus are responding to the disputes with.

In any-case, we’re pretty successful with the paid collections

Feel free to email me directly at [email protected]

Hello Ali – I have one account from Enerbank that the balance was paid all the way off, but they held .01 and insisted I had almost two months in late fees and charges. I wrote them several letters disputing the charges, but they just continued to send me letters saying I had not responded, and eventually charged it off. In addition, they are still reporting it 30 days past due, two years later, month after month. I have all the documentation of what they sent me, and what I sent them, in chronological order. Should I go ahead and file a credit bureau dispute letter and send all this documentation?

Hi Joel , yes that may be the first step. If that doesn’t work out file a CFPB complaint. And if the matter is still not resolved, then reach out to me for further help

I sent out your debt verification letter to the collections company. I didn’t send it to the credit agencies. They did get back to me and here is what they said. Basically, their letterhead says, “As you are already aware, ARS represents physicians who provide services in health care facilities throughout the country.” In response to your request for verification of the debt, we have listed the information below. ARS has verified this information with our client and confirmed the outstanding balance of $780. Below they list the physician/creditor’s name and account number, my name, the amount owed, and the service date, which states 1/20/2018.

I’m in South Florida and the debt is out of Broward County. I’m willing to pay a lump sum, but I don’t want to spend more than $250, and I want it cleared off my credit and not displayed as paid.

HI David, you can call the collector and see if they’ll come down on the amount and delete the account. You can tell them that you’re contesting this debt but in the spirit of compromise willing to settle. See what they say first and if they don’t agree to delete, then reach out to me using the link below : https://www.imaxcredit.com/consultation/

Good Ali,

I ran my credit report back in March and seen a lot of personal information and things on my report that I don’t recognize. I have an adult som with the same name who doesn’t use jr. I have been fighting the credit bureaus to get this stuff off and to validate the information they are reporting. All I get are statements. Which are from address that I have never lived at. What would you recommend to help get rid of all the erroneous items?

Hi Jae, what you’re suffering from is what they called a “merged file”. where the credit bureaus mistake you for someone with a similar name, as long as both of you lived in the same city.

We should be able to help. I just sent you an email to pick up the conversation, if you didn’t reveive the email , just fill this form out and I can call you : https://www.imaxcredit.com/consultation/

I have late on Comenity Bank showing on my report from this year . I have never been late before. I disputed it and I got a call from the attorney generals office saying that they can’t contact the bureaus but she emailed me my payment history with no late payments. How do I get this off my credit.

Hi Jimmmy, recent lates are not going to come off with credit bureau disputes.

However, I should be able to help with this , as my attorneys can take legal action against Comenity Bank.

Use this link to setup a free consultation with me: https://www.imaxcredit.com/consultation/

Hello there, does this letter work for Bank of America late payment removals?

I’ve tried disputing before and had no success with the bureaus.

The BOA late incurred very recently and my score has dropped over 100 pts

Hi Ali

I have a recent 30 day and 60 day late payment with American Express, I was in the middle of moving and wanted to see what to do to get this removed.

Hey Sandra, Amex will sometimes make exceptions for moving.

first thing is call their customer service dept (do not talk to their credit bureau dept.)

Tell them you were in the midst of moving when the Amex late payment occurred and make sure to tell them you had enough money to pay.

If they don’t agree to remove the late, then fill out the consult form here to setup a consult with me:

https://www.imaxcredit.com/consultation/

I have a question I have two negative items on my credit reports, one is a collection from Midland Credit and another from Portfolio Recovery, both of which I do not recognize.

What can I do ?

Hi Violet, glad you reached out, first send the collection companies this validation letter here https://www.imaxcredit.com/remove-collections-credit-report/, via certified mail . Basically in this letter, you’re asking the collection companies to send you proof of the debts, in the form of a written contract with your signature

Wait about 15 days and then send the three credit bureaus dispute letter to Experian, Equifax and Transunion.

If 30 days later the credit bureaus don’t delete the items and the collection companies haven’t provided you with validation of the debts.

Then lodge a separate complaint against each of the 3 bureaus and the 2 collection companies at http://www.ConsumerFinance.gov. (CFPB_

Which will be a total of 5 complaints. You can also lodge a complaint against all the parties with your state’s attorney general’s office.

Good evening Ali, I have a collection account on my credit report from 2017, never made a payment, sent a cancellation notice certified still have the green receipts when sent to the original creditor. In November I sent a certified letter to the collection agency which was returned to sender. How would I dispute this to have it removed? Thank you and God bless!

-Vicki

Who do you send the goodwill letter too ? I can’t find that information for NMAC (Nissan)

Hi Tamara, if you have a 30 day late payment with Nissan, please look into this article :https://www.imaxcredit.com/how-to-remove-a-30-day-late-payment-from-the-credit-report/

Hi Ali , I have recent 30 day late payments with Amex, Capital One , Comenity Bank.

You’re right in your article above that credit bureau disputes don’t remove recent lates.

Could you tell me what does remove lates?

Good morning Whitney,

So recent late pays, with any creditor won’t come off with credit bureau disputes nor goodwills.

There is a process for this, which requires more finesse,

Look at my article here on this, which gives you what’s involved.: https://imaxcredit.com/how-to-remove-a-30-day-late-payment-from-the-credit-report/

If this doesn’t help, then email me at [email protected] for a consultation

I’ve got a recently paid American Express Charge-off account. I’ve used dispute letters before that haven’t worked and even hired 2 credit repair companies and even tried Brandon Weaver’s youtube tips.

The Amex chargeoff was incurred about a year ago.

Will this dispute letter help?

Jennifer, firstly let me say I’m sorry to hear about the time and money that you’ve been robbed of.

Sadly this is the norm with the credit repair industry, it’s not the most ethical to say the least.

As for the American Express charge-off, credit bureau disputes are not likely to get this off, since the account is so recent.

Credit bureau disputes for charge-offs normally work for much older accounts, figure 4-5 year old accounts.

My contracted attorneys sue Amex quite often and we do engage their legal department frequently.

I’ve got a 90% deletion rate with Amex.

For a free consultation, reach out to me at my personal email at [email protected]

I moved from CA to TX in 2013 and have had no contact with 2 legitimate charge-off’s from CA water utility and PG&E since. Experian is now reporting the delinquency as 2014 for one, and 2015 for the other. Is that evidence of re-aging, and can I have the 2 negative entries removed for incorrect date of delinquency?

Hi Daniel, re-aging is not that simple to spot. Go to annualcreditreport.com and pull your reports from there. Those report formats will show you the date of fall off, and if the date of fall off is showing more than 7 years after 2013, then that is re-aging.

Now, with removing PG&E Collections, or utility bill collections, like Comcast collections, AT&T collections, it depends on who is reporting the account.

If the account is being reported by the original creditor then you can lodge a complaint with the public utilities exchange commission, if its being reported by a 3rd party collection company, like Enhanced Recovery, IC Systems or Midland Credit Management, then you need to lodge a complaint with the consumer financial protection bureau.

Hope this info helps

Hello. Transunion removed a old Verizon bill but Equifax and Experian wouldn’t. How can I get them to remove a dispute? they keep saying it’s still under investigation

Hi Carmella, the Transunion investigation normally takes 30 days, now if 30 days have passed, you can either call them. Also see if the Verizon collection is showing as “consumer disputes account” or is it showing as “account under re-investigation,” if its the latter this is a Transunion issue. Now if its showing just as “consumer disputes account” then you want to call the Verizon Collection department directly, tell them you have a Verizon Charge-off account you no longer want to show as disputed.

did not get an email from you Ali this is Andre

Andre, please check your spam folder, or email me at [email protected]

can you email me what I need to get going to hire you?

Done Andre

and I have one closed account who still reporting with interest on my credit each month ,will this still work on it too??

Hi Vincent Depends on how old the account is, look up the statute of limitations for debts in your state. If it’s within the statute then disputes won’t help and only settling would

I live in apartments building for 5years and after I move out they send me to collection for 1400 for nonsense (fixing stuff, carpet cleaning, trash)and they even keep my deposit…will this letter help me get that off my credit

See my post above to your prior question.

if the debt is within the statute, you’d probably need to file a complaint with the Dept of Justice against the landlord

Hello, I called experian to have my dispute comments removed from credit report. They had no problem removing them, however, there is a section on my credit report called “reinvestigation information” and it states “this item was updated from our processing of your dispute in January 2019”. I called experian back to tell them about it and they said that this was just referencing an old dispute but does not count as a dispute remark and should not prevent me from getting a mortgage. Is this true? He also said that this information could not be removed.

Hi Gabrielle, once a dispute is completed and it says , dispute resolved, the mortgage company should not have a problem with the dispute comment

Hello Mr Zane,

First off, thank you for sharing your valuable expertise in this area. It serves as a tremendous benefit to the public. My question relates to a collection item on my account. A utility company in NC sent me to collections for a final balance owed. I was not aware they would assess this charge. I moved to CA and received no past due or late notices. No mail, phone calls or emails were received. I didn’t realize there was an issue until I saw my credit score tank. I foolishly paid off the utility without negotiation in an attempt to have this removed. It did not get deleted and still remains as a detriment to my credit. Do I have any recourse besides waiting for 4-7 years?

Hi Ken, just emailed you with suggestions and questions.

Ali, this is the problem. My husband passed away 3 years age this Sept. I just found out that the home mortgage has not been reporting to the credit bureaus that I have been making the monthly payments. My husband’s name was first on the loan and mine was the second. I have talked the the mortgage company and I have to send a written letter to dispute this issue. will your letter help me with this

Hi Shelia, so saddened to hear about your loss. My thoughts and best wishes are with you.

As for the mortgage, first, find out if your name was on the loan, and not just title.

One way to find out is if the mortgage statements reflect your name.

Next if you’re dealing with a small mortgage company, unlike chase or boa etc, you want to find out if the mortgage company reports accounts they service to the credit bureaus.

Alot of smaller mortgage companies don’t even report, but the larger banks do.

Finally, you can lodge a complaint at http://www.consumerfinance.gov against the mortgage company, and someone at the mtg company’s higher management will communicate through you via the CFPB to resolve the issue

No Problem and Thanks Ali. So once the dispute is resolved equifax should remove the comment automatically correct ?. My dispute was resolved yesterday. I still see the comment in equifax report. So should I wait for few more days to reflect the same in equifax report? or do you want me to contact equifax?

Thanks once again for your help.

Do contact them, and talk to a live rep. They should be able to resolve the issue on the phone

Hi, i have a sba loans charged off on my report is it possible to get it remove

student loans like SBA loans, that are federally backed, these don’t go away unfortunately unless settled.

Thanks Ali for the quick response. Sorry I am not clear on the response. Do I need to explicitly contact equifax to remove the remark even though the dispute is resolved?

Sorry I misread your question earlier. Pull the latest credit report from Equifax to see if they’ve removed the account already.

If they haven’t then put in a dispute with equifax

Hi,

Any recommendation for disputing about 12 late payments (120 day lates) on three cards? This happened in early 2016 (just shy of the 4 year mark), and I settled each one for less and it is closed. I tried to buy my first home and these lates are making it impossible to get the loan I need. Since they are almost 4 years old, would you go straight to the credit bureau and dispute them? Any good dispute reasons? I just didn’t have any money to pay them at the time. Thanks and I love your site.

Hi Maria, yes, you’re better off just disputing the account and see what happens.

If you see that each of the 3bureaus are reporting different late payment dates, then you can try to dispute the accounts under the incorrect payment history

If they don’t come off with the dispute, then let me know and I can step in for some advanced intervention.

Hope this helps

Hi I’d like to have a model letter to credit inquiries

Hello, I assume you’re referring to a sample letter. You can use the sample letter here to dispute inquiries: https://imaxcredit.com/remove-inquiries-from-your-credit-report/

I’ve run into an issue with Cap One, who’s unwilling to remove their listing. How long will this take ?

Hi Amy, normally it would take about 45 days for the dispute to come back with a result

I’m a victim of id theft, a $1million mortgage was taken out in my name. what can you help with?

Hi Janice, check out this link below for Id theft help, I also offer a personalized service if you need a professional to help:

https://imaxcredit.com/how-to-repair-your-credit-after-identity-theft-and-fraud/

I just verified through my states attorney general’s office that a couple collection agencies that have entries on my credit reports for old debts are

not even licensed. The original debt occurred in my state. Any suggestions on how to proceed?

Hi Norm, we may have some options to pursue, you can email me the credit report at [email protected] so I can provide you with a free consulation

Could you please advise if the statute of limitations goes by the state you lived in at the time the debt was incurred, or the state you currently live in? For example, if you had an unpaid medical bill while living in California which has been turned into the credit bureau, but are now currently living in Minnesota? A four year statute of limitations, vs a six year, respectively.

My sincerest thank you for all the information you provide – absolutely priceless!!

Hi Cindy, the statute is based on where you live at the moment. So if you’re in MN , then the local statute there would apply

I’m in a debt settlement program regarding 4 credit cards. One has been paid, one is being paid, and the other two are still being negotiated. It has dropped my fixo score 200 points. I have no other debts and recently paid off my mortgage when I sold and moved out of state (also not helping my credit) I acquired a secured credit card to begin rebuilding. Is there anything a letter would help me with? The paid off credit card shows on my report as zero balance and the other 3 show as charge offs.

Hi Michelle, normally disputes are not effective for valid accounts that are unpaid, so once these accounts are paid off, then only would the creditor have no incentive left to verify and you’re better off disputing then.

If I have multiple closed accounts (6) on my credit report that are extremely past the States Statue of limitations ( one from 1999 ) would this letter work to help me start the process of removing them from my credit report? Thank you for your advice

hi Jacqui, this is exactly what it’s for.

Keep in mind the 7 year statute begins from the time of last payment. And the statute does not apply to any govt of state owed debt, like student loans, child suport etc, these don’t have a statute

Thanks for sharing! I will update with results after 30 days.

Terrific, best of luck Van !

Hey Mr. Zane, Whats the best way to get the dispute handled by a human and not the eoscar automated way?? Ive heard stapleing a lot helps and adding several pages to the letter so it takes longer to go thru. Thanks for the reply bud

Hi Mark, basicially, it will still be an e-oscar dispute but if you send in a mail request, then at least it will be manually inputted.

Can tax liens be expunged with this letter?

Fortunately, tax liens no longer show up on credit reports, but they do show up on court records.

Thanks your letter worked, I’ve been disputing a few accounts on my credit report for almost 2 years now, and today the last agency responded. All accounts were either corrected or removed. Thanks again.

What can I do to expunge incorrect addresses on my report?

Simply fill this letter out and send it to the bureaus with your latest address proof, id , ssn copy

Can I use this to remove inquiries ?

You sure can my friend, follow the instructions

I’ve had credit bureau disputes before with no results, what should I do ?

Hi Chaussure, yes sometimes we may need to look into more advanced options, reach out to me through the website and do let me have a look at your report, I’ll see what I can help with

Is there any way to dispute or remove a closed account with negative history from the credit report?

Can recent 30 day lates be removed with this letter Ali ?

Hi Jennifer, unfortunately 30 day lates require more advanced intervention, look at my other blog post for how to remove 30 day lates

Hello Ali, can you please update this to demonstrate how to remove inquiries ?

Hi Josh, I have a blog post and a special letter for that , refer to my blog page for that

The bureaus have put a fraud alert on my credit report, what can I do ?

hi Victor, use this letter and change the heading to request to remove the fraud alert, make sure to send in your id docs, this should do the trick in 30 days

Greetings Ali , my husband and I are looking to purchase a home and need our score increased asap, what can we do to expedite this ?

Hi Emily, thanks for reaching out, yes I should be able to help, use the contact form below and reach out to me

I have a recent late payment on my toyota auto loan that’s not coming off with disputes

Try calling the creditor, but first refer to this post and see how to approach it and let me know what happens:

https://imaxcredit.com/how-to-remove-a-30-day-late-payment-from-the-credit-report/

I’m trying to remove a fraudulent charge off account, what special instructions I need to follow?

Hi Billy, refer to my blog page, I have a separate blog post that deals with fraudulent items

Can I use this to remove old bks

Hi Irene, yes this would work for questionable bks

Hi!!

Which method would you recommend? I have two negative accounts on my credit report. One is a student loan, which I let default [after believing it was still in deferment] in 2016. Once I received the default letter, I immediately worked with the collection agency and started a loan forgiveness program where if I paid 9 consecutive on-time payments, in good grace they would remove my default status. I then set up automatic payments to the collection agency (and not the loan servicer) and completed that program. But during those 9 months of making the on-time payments, they all were marked LATE past 120 days. What’s the best way to go about disputing those late payments and have them updated? Is it possible to remove that account all together???

The second negative item on my credit report is an old Verizon account (from either 2013 or 2014). I let my account fall behind and my service was cancelled. Back then when I received my final bill, I saw a bogus equipment fee of $1200+ after returning all equipment. My credit wasn’t much of a concern to me as much as it is now so I said to myself there’s absolutely no way I’m paying them so I left it alone. Since then, a collection agency bought that account and is reporting on my credit report (since 2016). Any advice on getting that account removed off my credit report all together? What would be the best way of accomplishing that? I don’t know the exact date this account will age off because the collection agent states 2016 as the original date on my credit report (although I haven’t had Verizon since either 2013 or 2014).

Any advice would be greatly appreciated 🙂 Thank you.

(From New York)

Hi Charlene, for the student loans write to the CEO of the student loan company and ask they remove the late payments, given you were in a rehab program and lates should ahve been removed.

For Verizon, you’ll need to file .a regulatory complaint against them, try the public utilities exchange or the BBB even

Hope this info helps

Hi,

I sent my dispute letters to the Credit Reporting Agencies certified mail. I have not received anything from the Agencies but, I received a letter from the collections consumer. Why did I receive a letter from the collections costumer and not the credit reporting agencies? The letter stated I didn’t provide enough information and they couldn’t investigate it. I clearly put on the letter that I wanted the original contract. What do I do next? send a second letter?

Hi Latiya, the bureaus are not the ones to send you the contract, only the original creditor or the collection company can. You’ll need to send the collection agency this letter in this blog post below: https://imaxcredit.com/remove-collections-credit-report/

Thanks Ali for the all the info, for my case I have 3 late payments with two different credit cards and about 13 hard inquiries how do i go about disputing these?

Hi Bantar, just shot you an email with some more details.

It’s hard to come by educated people in this particular subject of disputes, but you sound like you know what you’re talking about! Thanks for spreading the knowledge

Thanks for the kinds words Tammy, hope this info was helpful to you!

Excellent article. I certainly loved all the info you shared. Continue the

good fight against the credit Bureaus !

Much appreciated Marcus !

Ali , what will get me better results ? mailed or fax disputes?

Hi Sally, the results won’t be different, but faxed disputes may shave a few days off the investigation period.

Woo hoo!! Got 4 of my negative accounts deleted using this letter for Equifax, thanks so much for sharing this information Ali !!

Terrfic news Cecilia, super happy for ya and thanks for the kind words !!!

Hello, I’ve tried disputing multiple times with Experian and they refuse to remove a frivolous Bank of America mortgage account from the credit report, what options do I have?

Hi James, try lodging a complaint against Experian and against Bank of America with the Consumer Financial Protection Bureau at consumerfinance.gov, this should do the trick

I have multiple reason lates that I have disputed but they do not come off, what would you reccomend ?

Hi Gregory, please refer to this blog post on how to remove recent lates :https://imaxcredit.com/how-to-remove-a-30-day-late-payment-from-the-credit-report/

Can I request the bureaus to block my file to keep from creditors to report accounts ?

HI Gregory, that’s not recommended, a block would only stop someone from accessing your credit report, and not keep a creditor from reporting .

Hello, my credit report is mixed with my dad who’s got a similar name, his accounts are showing on my credit report, can I utilize this letter to fix the problem ?

Thanks for you help

Hi Donald this is a common problem, to answer your question, add a paragraph on top of the letter, stating you have a merged file, and clearly state your dad’s name and dob as well as yours, if you know your dad’s ssn, put that in there too and tell them to “unmerge” the two files. The bureaus think that both you and your dad are the same person, so they need to be given evidence that you are not.

This should fix the problem

Awesome article Ali, and thanks for sharing the secrets of the credit repair world!

Thanks for the encouraging words Wendy !

I have been browsing online more than 3 hours today for credit repair help and am really glad I came across this letter.

I wanted to ask how frequently can this letter be used

Hi Jerry, the bureaus can turn down your request to investigate if you do not wait 30 days after the completion of a prior dispute. In other words wait at least 60 odd days after you send in a dispute to send in another one

Such a great resource for credit improvement, thanks so much for sharing this with us folks Ali !

Hi Ali , I have a late payment on my Capital One account, I’ve already disputed online, will this letter be helpful?

HI Mary, late payments require a different strategy, read this blog post regarding how to remove them: https://imaxcredit.com/how-to-remove-a-30-day-late-payment-from-the-credit-report/

Reach out to me if you need help removing it.

Best

Ali

Ok, so what is your take on fax disputes instead of mail disputes ?

Hi Kyra, fax disputes are fine as long as you get a delivery confirmation , which is key. We need to have proof that the disputes were delivered in the event the credit bureaus need to be taken to task for non-compliance.

Hello Ali, I’ve already disputed online before with the credit bureaus, can I redispute again ?

Hi Johanne, thanks for sharing and reaching out. Yes, you can I would recommend waiting at least 30 days after a dispute has been completed and then disputing. The bureaus can legally turn down your dispute if you do not wait a month after the completion of prior disputes. I would also recommend disputing the address linked to the particular questionable accounts to ensure a higher deletion rate.

Hi Mr. Zane, I had a fraudulent charge-off showing on my credit report , would these letters work for that and any other special instructions I need to follow?

HI Nicole yes those could work but you’ll need to file reports of the fraud incident reports with the local police and the FTC online as well, and send those reports to the bureaus along with those filed reports

I was trying to get approved for business financing and they turned me down due to excessive inquiries. Will credit bureau disputes work for those?

Hi Ava, for those you can use the instructions and sample letter I’ve included in this blog post: https://imaxcredit.com/remove-inquiries-from-your-credit-report/

I have tried several times to dispute a collection account with a credit bureau but it hasn’t helped , the account is from 2017 from a doctors visit, what other options do I have ?

Hi John, if you’re in California, then creditors legally have 4 years to collect on debts and credit repair disputes aren’t affective for recent collections.

You’d be better off settling in exchange for deletion, however, the key is to get the item deleted and not to have it updated as paid. I’ve got a blog on this that shows you how to do this:

https://imaxcredit.com/how-to-delete-a-collection-exchange-for-payment/

Hope this helps

I can not thank you enough for the information you’ve provided to people, like myself, who are simply are unaware on the proper procedures to utilize when dealing with the credit bureaus and/or businesses in regard to dealing with inaccurate information, or those of us who may have went through a difficult time, and want nothing more than to repair our credit – but simply aren’t sure which is the best course of action to take. I’ve been up all night thoroughly reading and taking notes on every bit of information you’ve provided. Knowledge is power – I can’t thank you enough!

Gald this is helpful, wishing you the best !

The topic of credit requests remains for me something that is not fully understandable and complex, as I have never been able to find answers to many questions. Are you recommending that removing dispute comments is something everyone should do?

Hi Heather, you should, by all means, remove dispute comments if they are on showing on accounts with a positive history. As for the comments showing up on any negative accounts, remove those only if a lender asks you to as part of conditions for an approval.

Howe this answers your questions

Very interested in utilizing this letter. How long do the bureaus have to respond back ?

Hi Jason, once the letters are received from the bureaus, they have about a month to respond back, but I’ve seen they complete their investigation normally within 14 days.